Böll EU Brief

Small modular reactors – smaller regulation?

Böll EU Brief 01/2026

Key findings:

-

The term small modular reactors (SMR) is not standardised, and SMR concepts are not small. Instead, the capacities of many designs are comparable with nuclear reactors built in the 20th century.

-

Technically, most SMR concepts do not differ from existing light water reactors. Current assessments show that their reduced capacity does not automatically reduce the risk of accidents. Instead, their heterogenous nature requires specialised infrastructure for fuel production and waste management that does not exist today. SMR concepts designed to operate on high-assay uranium could even increase nuclear proliferation risks.

-

There is a hype around SMRs – this is problematic because of the many open questions and risks. The heterogenity of SMR concepts hinders mass production and consequently, envisioned cost reductions. Most SMR concepts remain in early design stages and are yet to receive regulatory approval or begin corresponding processes in the EU. Once these steps have concluded, additional site licensing, construction and comissioning steps would still be required. Electricity production from SMRs is unlikely to materialise at scale in the near term and remains decades away. If it occurs, it will come at very high costs.

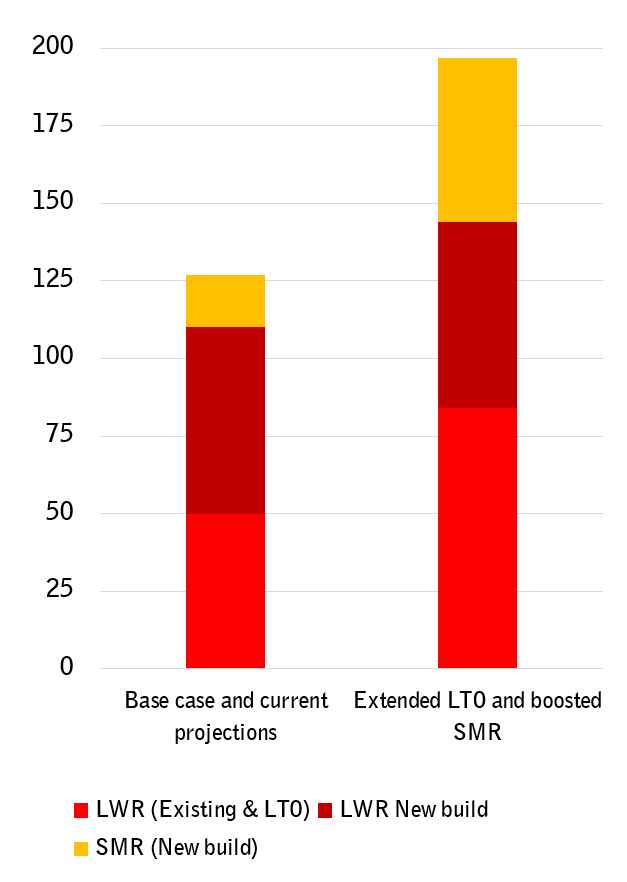

The hopes associated with the development of SMRs became evident when in June 2025, the European Commission presented its 8th Nuclear Illustrative Programme (PINC). It called for investments exceeding EUR 240 billion until 2050 to achieve the Member States’ nuclear expansion plans.

According to the PINC, so-called SMR concepts ‘could serve as complement to renewable energy’ by ‘[helping to] achieve an integrated, secure, stable, high-efficient and resilient energy system’ via flexibility provision, co-located electricity and heat generation, and hydrogen production.1

Furthermore, claims of new SMR capacity ranging from 17 to 53 gigawatt (GWe) were made, in addition to ambitious claims of high-capacity reactor new build and lifetime extensions of existing plants.

This would potentially double the EU’s current capacity of 86.6 GWe to 125 GWe or even 197 GWe by 2050 (Figure 1) – despite aging fleets, limited active construction and decade-long lead times for new nuclear projects.

The ongoing enthusiasm regarding the expansion of data centres for cloud computing and AI is further fueling this hype around SMRs that they could ‘provide a source of baseload low-emissions electricity’.2

Figure 1: Envisioned capacity development to 2050 (Installed capacity in GWe)

These optimistic claims stand in contrast with actual industry potential and various risks associated with nuclear power plants. At the time of writing in February 2026, no SMR concept had been granted a construction licence in the EU. The only SMR concept with ongoing construction activities outside of Russia and China, the GE-Hitachi BWRX-300 reactor in Canada, is yet to begin pouring concrete for the reactor housing, and all other concepts remain in early development stages, thus owing proof of the PINC’s claims and placing their potential useage many years into the future.3 Taken together, this raises critical questions about the realistic role of SMRs in the EU’s strategy. We therefore provide a brief overview of the current state of SMR concept development and highlight some of the remaining challenges.

What are SMRs?

Originally, the term SMR was used in the industry to designate small- and medium-sized reactors. This covered the “natural” development from research reactors and demonstrators with low power (< 100 MWe) to larger units of several hundred megawatts (MWe) to exploit economies of scale.

The term SMR was re-coined by then-US Secretary of Energy Steven Chu in 2010 in an attempt to relaunch a previously failed “renaissance” in the early 2000s. Therefore, today, the term SMR usally incorporates reactors with less than 300 MWe of electrical capacity, although some concepts exceed this arbitrary limit by quite a margin, for example, the Rolls-Royce SMR with 470 MWe.4

The collective term SMR can incorporate a vast array of different reactor technologies, such as light-water reactors, high-temperature-gas-cooled reactors, reactors operating on fast neutron spectra, molten salt reactors, and more. Each of these technologies implies the use of technology-specific supply chains and fuel-cycle arrangements, as well as distinct approaches to decommissioning and waste management. Further, most concepts remain in early development stages.4-6

How close to market introduction are SMRs?

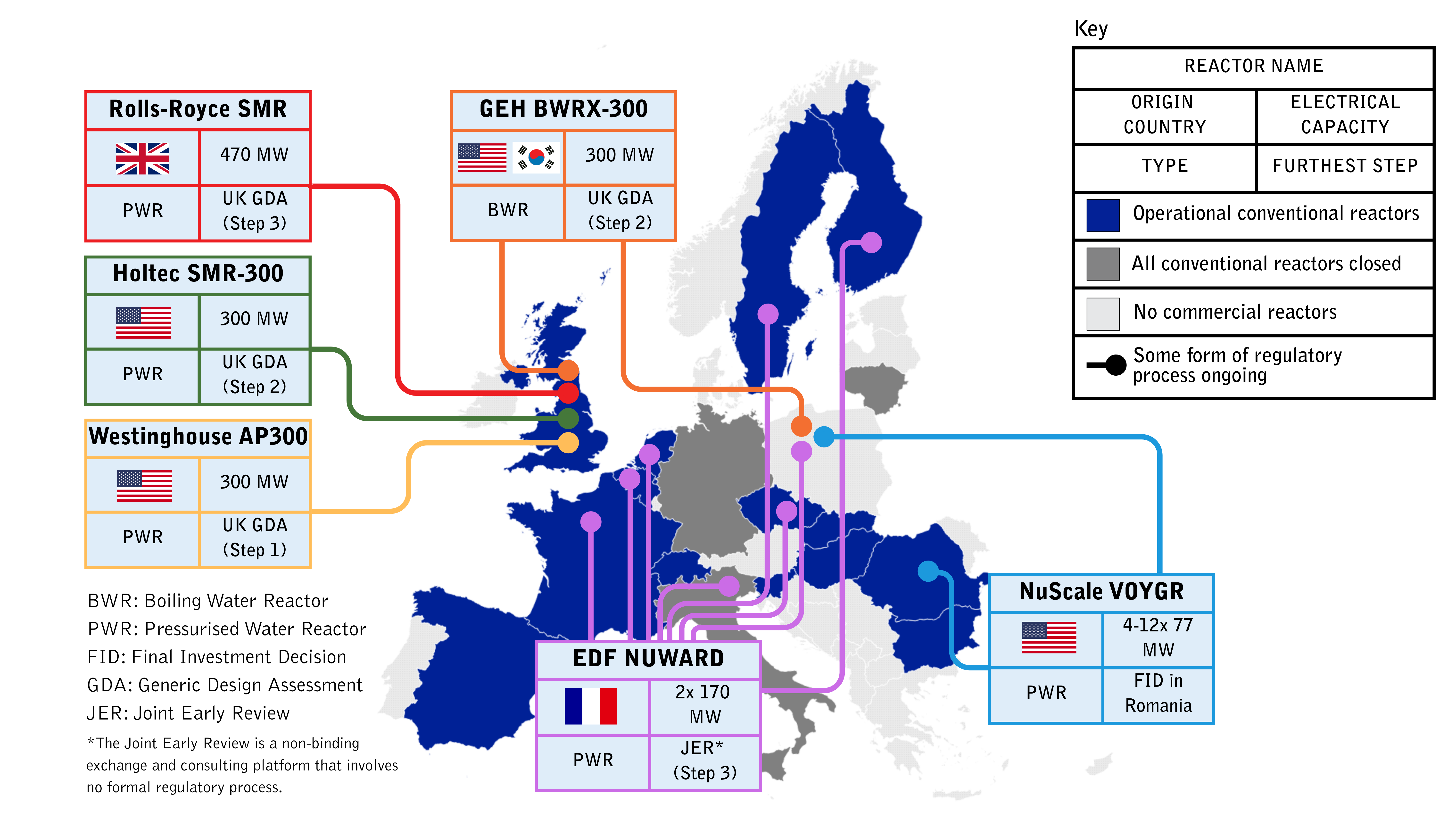

Most concepts are in early development or licensing stages. For example, the NuScale VOYGR was granted a standard design approval by the US Nuclear Regulatory Commission (NRC) in May 2025 and is undergoing a licensing process in Romania. While a final investment decision (FID) was reportedly made in February 2026, there is currently no ongoing construction project. The Rolls-Royce SMR has reached the third and final step of the UK’s Office for Nuclear Regulation Generic Design Assessment (GDA). But it is still waiting for site licence approval to begin construction. Several other designs are in various stages of the GDA process. The Argentinian CAREM reactor, under construction since 2014, was abandoned in 2024, and a new design is being sought, albeit with an uncertain timeframe. The French NUWARD concept is undergoing a redesign process aimed at increasing its electrical output to around 400 MWe, requiring licensing process restarts. Outside Russia and China, whose individual SMR prototypes are operating, with, from what is known, meager performance indicators,7 the Canadian project at Darlington, Ontario, represents the most advanced case, although only one of four originally planned GEH BWRX-300 units received a construction licence in May 2025.

Figure 2 shows some of the SMR concepts currently under development and their respective furthest regulatory process steps. Ongoing activities in respective countries are indicated by the coloured lines, such as the Joint Early Review (JER) for the NUWARD reactor. However, the JER is a non-binding communication platform between several European regulators and indicates no actual licensing activities. To conclude, most SMR concepts are yet to gain regulatory approval in the EU or even begin actual licensing processes. They are thus far away from a broad market introduction.

Figure 2: Overview of ongoing licensing or review activities of SMR companies in Europe

Major challenges for SMRs in Europe

Technical challenges

Broadly speaking, the proposed SMR concepts do not represent technological breakthroughs, but the smaller size is intended to provide increased safety performance. While some concepts bank on innovative passive safety systems, like the NuScale VOYGR, the LWR technology itself does not fundamentally differ from today’s fleets, bringing similar or potentially additional safety-related risks. Regarding other reactor technologies, like high-temperature reactors or fast neutron reactors, experience with now closed prototypes is dominated by emergency shutdowns, as well as safety- and cost-related project cancellations.5

Recent expert assessments conclude that it is not possible to state that SMR concepts generally achieve a higher safety level than high-capacity reactors. These assessments indicate that, contrary to some developer claims, emergency planning zones are likely to remain necessary for SMR concepts. Furthermore, radioactive release potentials have not been fully assessed, and the implications of modulary installed reactors at a single site remain uncertain.5

A central promise of SMR concepts is the potential to benefit from industrial learning effects through serial production and standardisation. However, this presupposes the repeated deployment of a limited number of standardised designs. The current SMR landscape is instead characterised by heterogeneous reactor concepts based on different technologies and design philosophies.

The International Atomic Energy Agency (IAEA)’s Advanced Reactor Information System lists more than 70 SMR designs, of which, according to the IAEA itself, many neither fulfil modularity requirements nor are expected to reach commercial readiness.

Implementing various nuclear technologies would require suitable and customised supply chains due to heterogeneous fuel requirements, for example, different enrichment levels for specialised fuel. Different reactor concepts would also generate different types of waste that require specialised infrastructure.5,8

There are also open questions regarding the suitability of SMRs for decarbonised industrial heat provision. Most industrial processes require temperature levels that can be easily provided by industrial scale heat pumps, or direct electrification. But only high-temperature reactor concepts could theoretically provide the heat of up to 1000°C required for steel and glass manufacturing for which low-carbon alternatives exist today–and most SMR concepts are light-water based.

Economic challenges

Economically, SMRs are unlikely to become competitive with existing gigawatt-sized reactors. The economic case of SMRs centers on scalability and modularisation. In contrast to consumer technologies, like smartphones or computer chips, nuclear reactors are capital-intensive assets whose costs are dominated by construction, regulatory compliance and financing rather than component manufacturing.

Calculations indicate that hundreds to thousands of reactors of the same design, vendor and capacity would need to be manufactured to achieve cost levels comparable to those of current high-capacity light-water reactors;9 SMRs will thus be more costly than large reactors per unit of electricity.7 The substantial cost reduction assumptions are often included in energy modelling scenarios that result in substantial nuclear capacity expansion expectations.

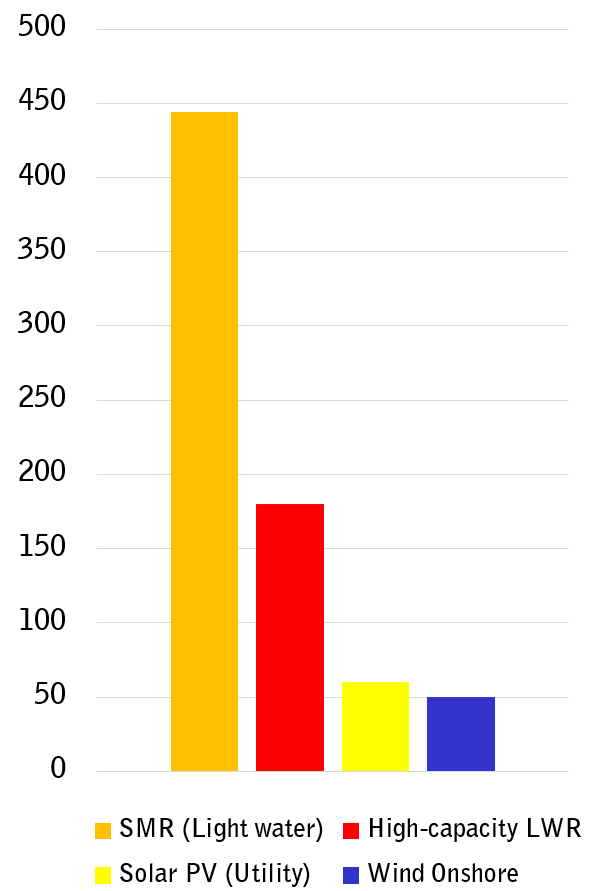

In practice, current deployment trajectories provide little evidence that such manufacturing volumes are achievable. The BWRX-300 project in Canada is estimated to cost at least CAD 7.7 bn (EUR 4.76 bn or 15,870 EUR/kW) for a single reactor as of May 2025. There is substantial doubt on whether localised manufacturing facilities (and thus reduced costs) will materialise.7 Historically, the nuclear industry has tended to increase rather than reduce costs.10 Figure 3 shows current levelised costs of electricity (LCOE) for existing technologies, and the mean projected LCOE for light-water SMR concepts. These figures do not include additional costs for infrastructure expansion caused by grid integration of SMRs or flexibility measures for fluctuating renewables, or costs for nuclear waste storage.

Furthermore, the economic case for heat supply from SMRs remains weak.11 Recent studies indicate that SMRs would, at sufficiently low costs, still induce higher overall system costs than lower-cost alternatives capable of delivering the same service today, such as large-scale heat pumps or direct electrification.12

Finally, integrated energy system modelling suggests that SMR concepts will have to deliver on their cost promises to become relevant in a future European energy system.11 This is consistent with earlier research demonstrating the poor economic performance of nuclear new build in competitive electricity markets and studies highlighting the lack of economic necessity for baseload generation in mostly renewable power systems.10

Political challenges

The heterogeneity of SMR concepts will complicate their implementation in Europe, given the necessity of tailored regulation for different technologies and use cases, for example, emergency planning zones. Such requirements complicate siting decisions and regulatory coordination across Member States and could also hinder data centre or industrial co-siting as well as district heating.

Further challenges lie in the necessity of specialised waste management infrastructure. Given the lack of adequate waste repositories for Europe’s existing spent fuel from currently operating reactors, this issue must be resolved before implementing SMR fleets with heterogeneous waste streams.13 This raises questions of legitimacy, public acceptance and institutional credibility. Uncertainty regarding future disposal concepts, responsibilities, and long-term commitments constitutes a governance risk, particulary where repository strategies were developed for existing (light-water) fleets.

Additionally, specialised fuel requirements, such as designs relying on high-assay low-enriched uranium (HALEU) fuel, could increase proliferation risks and raise concerns about fuel supply security and international oversight.14

Many EU policymakers currently perceive SMRs as an additional promising option that could contribute to the EU’s emission reduction targets. However, even under very optimistic assumptions for the speed of market introduction of SMRs, they will likely not contribute to these political objectives before the 2050 climate neutrality benchmark. Thus, betting on near-term SMR deployment for decarbonisation binds limited political and administrative resources at EU and Member State level that could be better applied to existing cost-competitive technologies, namely, renewables and storage, to supply clean and affordable energy instead of waiting for a technology whose feasibility remains highly uncertain.4

Figure 3: Current and projected levelised cost of electricity for different technologies in USD(2022)/MWh

Conclusions and policy recommendations

After several failed attempts at a “nuclear renaissance” since the mid 1970s, the current hype about nuclear power plants with low capacity, also referred to as “small modular reactors”, is yet another attempt to save an aging industry in decline.

Based on current evidence and development status, SMRs are unlikely to provide a meaningful contribution to European energy system decarbonisation within a relevant timeframe. Instead, continued attention towards their potential benefits will decellerate the necessary transformation of the energy system even further. New designs do not fundamentally mitigate the inherent challenges associated with nuclear power, namely waste management, proliferation risks and high cost.

Furthermore, the heterogeneous nature of proposed SMR concepts creates regulatory, industrial and governmental complexities that increase the uncertainty regarding future cost reductions and large-scale deployment, while requiring the implementation of customised infrastructure for fuel supply, waste management and so on. Consequently, current capacity projections based on SMR deployment are highly unlikely. The EU should not wait until first SMR concept prototypes are built and – perhaps eventually – brought to scale.

EU policymakers should instead prioritise policy frameworks that accelerate the deployment of mature, cost-effective low-carbon technologies. This includes facilitating efficient grid utilisation, strengthening system flexibility and demand-side management, supporting decentralised renewable generation, and advancing electricifation of energy demand. Given binding climate targets and rising electricity demand, decarbonisation efforts must deliver measurable results within the current decade. In this context, relying on technologies that remain at early stages of development and require substantial scaling before delivering system-level impacts at very high costs entails signficant strategic risk and should be avoided.

Endnotes

1 European Commission. 8th Illustrative Programme for Nuclear (PINC) (2025).

2 IEA. Energy and AI (2025).

3 Schneider, M. et al. The World Nuclear Industry Status Report 2025 (2025).

4 Böse, F., Wimmers, A., Steigerwald, B. & von Hirschhausen, C. Questioning nuclear scale-up propositions: Availability and economic prospects of light water, small modular and advanced reactor technologies. Energy Research & Social Science 110, 103448 (2024).

5 Pistner, C. et al. Analysis and Evaluation of the Development Status, Safety and Regulatory Framework for So-Called Novel Reactor Concepts (2024).-

6 Wimmers, A., Böse, F. & Von Hirschhausen, C. Nuclear Physics and Reactor Technologies (Fission and Fusion). in Nuclear Power (eds Wimmers, A., Böse, F., Kemfert, C. & Von Hirschhausen, C.) p. 11–54 (Springer Nature Switzerland, Cham, 2026).

7 Friess, F., Siddiqui, M. & Ramana, M. V. Small modular nuclear reactors for developing countries: Expectations and evidence. PNAS Nexus 5, pgag006 (2026).

8 Krall, L. M., Macfarlane, A. M. & Ewing, R. C. Nuclear waste from small modular reactors. Proc. Natl. Acad. Sci. U.S.A. 119, e2111833119 (2022).

9 Steigerwald, B., Weibezahn, J., Slowik, M. & Von Hirschhausen, C. Uncertainties in estimating production costs of future nuclear technologies: A model-based analysis of small modular reactors. Energy 281, 128204 (2023).

10 Göke, L., Wimmers, A. & Von Hirschhausen, C. Flexible nuclear power and fluctuating renewables? — An analysis for decarbonized multi-vector energy systems. Energy Strategy Reviews 60, 101782 (2025).

11 Wimmers, A., Böse, F. & Göke, L. Can They Compete? Cost Competitiveness of Non-Light-Water Reactors for Heat and Power Supply in a Decarbonized European Energy System. Under Review at Applied Energy. Preprint at https://doi.org/10.48550/ARXIV.2412.15083 (2025).

12 Satymov, R. et al. Who will foot the bill? The opportunity cost of prioritising nuclear power over renewable energy for the case of Finland. Energy 337, 138630 (2025).

13 Ahlswede, J., Graefje, J. & Schopmans, H. Disposal of High-Level Nuclear Waste: Global Status and German Experience with the Unresolved Liability of Nuclear Energy. in Nuclear Power (eds Wimmers, A., Böse, F., Kemfert, C. & Von Hirschhausen, C.) 447–481 (Springer Nature Switzerland, Cham, 2026). doi:10.1007/978-3-031-99894-2_16.

14 Kim, P. & Macfarlane, A. Challenges of small modular reactors: A comprehensive exploration of economic and waste uncertainties associated with U.S. small modular reactor designs. Progress in Nuclear Energy 190, 105989 (2026).

Webinar recording

Small modular reactors - smaller regulation? - Heinrich-Böll-Stiftung European Union

Watch on YouTube

Watch on YouTube